1. Murray Dawe's (Slipstream Trader) outlook for the ASX: 29th July 2011 - Slipstream Trader Market Update

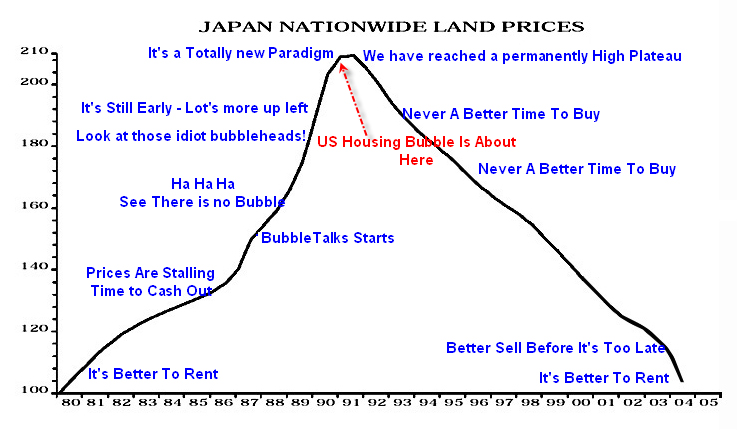

2. Peter Brandt's scary post on Head-And-Shoulder Techs and the possibility of 75% declines in the NYSE (hat tip to Avidchartist): Charts indicate a 75% decline in the U.S. stock market is possible

Jesse's notes (if you scoff at such declines):

- Christmas 1989, Nikkei 225 (Japanese Stock Index) tops at 38,916

- August 1992 - 14,820 Down 62% off peak in 30 months

- June 1995 - 14,517 Down 62.7% off peak in 5 years and 6 months

- October 1998 - 12,879 Down 67% off peak in 8 years and 10 months

- April 2003 - 7,874 Down 79.8% off peak in 13 years and 4 months (BINGO!!)

- February 2009 - 7,568 Down 80.6% off peak in 19 years and 4 months (BINGO MkII)

- Today (29th July 2011 close) it sits at 9,833 in 21 years and 7 months since its peak, its down 74.7% since peak (BINGO Mk III).

(The stock part of the chart below only goes to early 2008 before the GFC kicked off but it paints a trend)

3. Mike Shedlock on Cap-and-Trade: New NASA Data Blow Gaping Hole In Global Warming Alarmism; Idiocies of Cap-and-Trade Exposed

4. Bloomberg on one of the [many] holes in the Euroidiots 'solution' last week: Greek Bondholders May Shun Rescue as Potential Losses Top 21%: Euro Credit

5. Crude Oil in Australian Dollars over 3 months, 15.5% declines (anyone noticed a 15.5% decline in petrol prices? Me neither); $WTIC:$XAD - May, June, July