The REIV has surrendered in their latest blurb here .

The Melbourne median house price for the March quarter is $565,000, according to the latest results from the REIV. This represents a six per cent reduction from the revised December quarter median of $601,000.

REIV CEO Enzo Raimondo said, “it is evident that the current residential market in Melbourne and Victoria has entered into a different phase of lower transaction numbers and reduced price growth.

Reduced price GROWTH? Minus 6% a quarter makes the crashes in Spain, Ireland, USA look like benign easing. String together 11.2 quarters of -6% and in October 2013 your house is half in value.

The bogan rags are foaming a little as well in an article yesterday Melbourne property prices plunge.

MELBOURNE'S property bubble is bursting, with $400 a day wiped off the average house price in the past three months.

After peaking at $601,000 late last year, the median price has fallen to $565,000 - down $36,000. The 6 per cent slump is the biggest quarterly drop in more than two years and one of the biggest the Real Estate Institute of Victoria has recorded since the height of the global financial crisis.

So Melbourne is joining Hobart, Brisbane (all of QLD actually) and Perth, which had falls according to RP data.

That 2nd green 'hump' of positive returns is all Rudd/Swann FHOG boost. Your taxes inflating a bubble.

The Courier Mail (auxiliary toilet tissue used north of the Tweed R.) had some blurb about SE Qld house prices falling at the rate of 1.25% per month. I raise eyebrows and think, hell, that's bad. Yet some idiot writes in and says -1.25% a month is nothing and his investment is safe.

At this point I spray coffee onto laptop. It then dawns on me, we are a nation of the quite stupid (how could one govt after another get away with the shit they do). I remember a study done a few years ago confirmed this and after clicking and googling I finally find it.

Literacy and Numeracy 2006 (Adult Literacy and Life Skills Survey)

Prose

What does it mean? If you use long words, require analytical thought, or any numerical reasoning such as percentages, rates of growth/decay (eg falling house market) over 50% of Australians are not going to get it.

Read it and weep:

Australian Core Skills Framework (examples of 'level' skills at bottom of page)

Now this sits well, logically, with the demographic that actually buy investment property, those that think getting 4% yield (after expenses) on money borrowed at 7% is a good idea.

These folk:

Back to the -1.25% a month and the village idiot who claims that's nothing to worry about.

In 12 months. -14% off your "asset" (well the banks if you are mortgaged)

In 24 months. -26%

In 36 months. -36.4% (now Mr Nothing-to-worry-about is soiling himself and realises he holds a toxic lemon with a gabled roof).

Time to halving in value? 55 months and 3 days (4 years and 7 months). Oooooh that's about how long it took for Dublin prices to halve.

This doesn't account for inflation for we could possibly be in a deflationary spiral by then.

Now whose asset is it. If you have put down a 70% deposit and prices fall 30%, you've lost the lot and the bank's asset is still safe (your debt), if you stop paying because of 'circumstances' it will be a foreclosure sale and you are on the street.

If you borrowed 95% using mummy and daddy's equity and Rudd's icecream, a 30% fall is a serious bank problem. You are in the hole for over 6 figures and technically bankrupt but the bank is holding a loan backed by a lemon.

What of the slick dude who bought a house in 90s went to a seminar and using equity bought 2 investment properties, then 4, then 8. A 30% correction and he is toast, the bank is now having a collective thrombo.

I could have just wrote 'what happened in Ireland (or Spain or USA)' but what the hell.

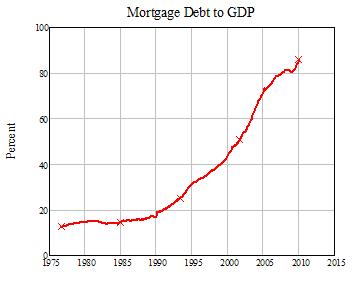

Now Australia's GDP is around $1.2Trillion, and if Australia's mortgage debt around 85% of that (this just amazes me everytime I see it, not just how stupid are the populace but how slick are the banks and govt playing the stupidity for all its worth)...

I calculate that a cool $1,000,000,000,000 ($1T) is mortgage debt.

Now a 30-40% correction in the housing marked takes out YOUR equity first, then the banks, how much of a hole will that put in banks balance sheets? $100B? $200B?

Who do you think will pay for a $200B bank bailout? You got it.

Tasmanian Real Estate Trouble on Wednesday posted a startling article titled "Business" where he outlines just how far, deep and wide the tentacles on this monster reach into the small business community.

Let there be no doubt, when she goes 10% unemployment in this country will be a 'good set of numbers' (consider Spain's 19% and Ireland's 14.7% which was 4.5% before the housing crash).

USA:

Australia's Economic Model:

No comments:

Post a Comment