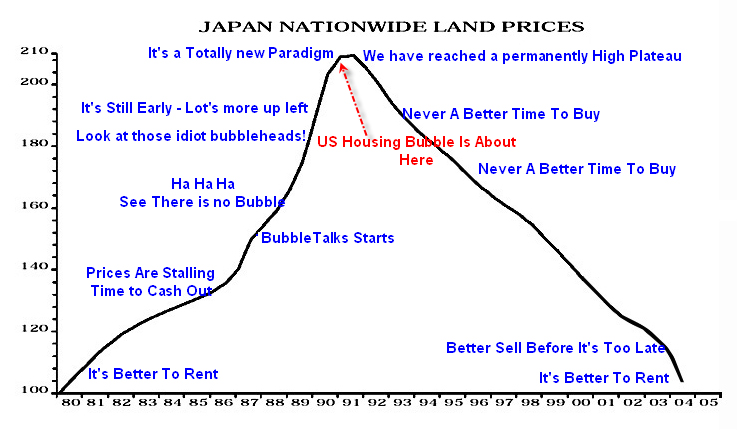

First, lets roll back the clock....

March 26th 2005; Its a totally new paradigm.

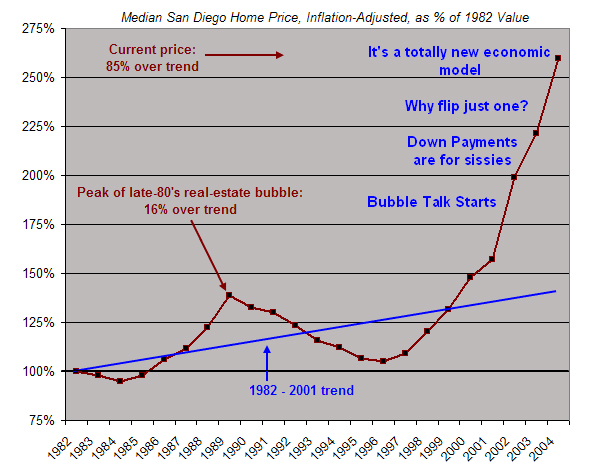

Quotes from 2005.

Ron Shuffield, president of Esslinger-Wooten-Maxwell Realtors says that "South Florida is working off of a totally new economic model than any of us have ever experienced in the past." He predicts that a limited supply of land coupled with demand from baby boomers and foreigners will prolong the boom indefinitely.

"I just don't think we have what it takes to prick the bubble," said Diane C. Swonk, chief economist at Mesirow Financial in Chicago, who was an optimist during the 90's. "I don't think prices are going to fall, and I don't think they're even going to be flat."

How did those markets go?

That new paradigm in Southern Florida of limited supply of land coupled with demand from baby boomers and foreigners [that] will prolong the boom indefinitely saw 55% falls in 34 months.

Roll forward 6 years to the Weekend's Mexican Bogan Rag, The Herald Sun. What a headline.

Decade of pain for Melbourne's property market

Deluded Quasi Pessimist:

The good news for homeowners is that AMP Capital chief economist Shane Oliver and Grattan Institute program director Saul Eslake - the ANZ's chief number cruncher for close to 14 years - say Victoria will avoid a US-style property crash which saw prices plunge by 30 per cent.

Instead, house prices will continue their single-digit slide into 2012 before stagnating for five to 10 years as wages catch up with a median house price which has climbed 133 per cent since 2000.

"We are facing a situation where we are just spinning the wheels for up to 10 years until incomes catch up with property prices," Mr Oliver said.

Deluded Industry Vested Interest Spruiker:

The Housing Industry Association's chief economist Harley Dale said price growth was likely to track inflation over the next 10 years. "That means you are not talking about any real growth," he said.

FAIL boys FAIL. History has shown it never happens. I wrote about this in April under History Never Repeats. Where Reinhart and Rogoff analyse 800 years of Markets....

The authors present eight centuries of financial folly, demonstrating the common theme that excessive debt accumulation regardless of the source — government, business or consumer — poses greater systemic risks than it seems at the time of the boom. (MoneyWatch recently interviewed Reinhart for her views on the current state of the economy.)

- Infusions of cash make a government look like it’s providing greater growth than is actually being provided.

- Private-sector borrowing binges inflate housing and stock prices beyond sustainable levels and make banks seem more stable and profitable than they really are.

- Large-scale buildups of short-term debt make an economy vulnerable to crisis of confidence.

They demonstrate that financial crises are protracted affairs that share three characteristics:

- The aftermath of banking crises is associated with deep declines in output and employment. Unemployment rises an average of 7 percent over cycles lasting more than four years on average. Output falls more than 9 percent over two-year periods, and it has taken about four-and-a-half years for output to fully recover.

- Government debt surges an average of 86 percent in real terms. The main cause is not spending but a decline in revenues

The bottom line is that the aftermath of crises has a deep and lasting effect on asset prices, output and employment. Unemployment increases and housing price declines have extended for five and six years, respectively. The authors also note that V-shaped recoveries in equity prices are far more common than V-shaped recoveries in real housing prices or unemployment. (2009 is certainly not an exception.)

IT IS NEVER DIFFERENT.

To cap it off the industry is as straight as a $3 note. A shining example of the fear, the dishonesty and total disrespect for buyers and the market: Agents withold house price data.

MELBOURNE real estate agents and vendors are increasingly withholding or manipulating data provided to the Real Estate Institute of Victoria, prompting calls for the mandatory reporting of all property sales to protect consumers.

A Sunday Age investigation has found that 27 per cent of all auction results published by the industry body in June were missing critical information - including the sale price, passed-in price or the reserve. Many auctions were not reported at all, distorting clearance rates that are used by buyers and sellers to gauge market strength.

Last month, agency RT Edgar sent a newsletter to clients warning there was a ''serious question mark'' over media reporting on the market because many agents were withholding sale prices and passed-in results. RT Edgar director Michael Ebeling said agents who were doing the right thing were being disadvantaged

because their competitors' clearance rates seemed better because they withheld information.

''We cannot see how the media is getting reliable sales statistics, and as a result are reporting misinformation about the market,'' the email said.

Despite conceding that the reporting system is a ''bit rubbery around the edges'', the Real Estate Institute of Victoria has refused to back calls for compulsory reporting of all auction results.

''It is not the role of the REIV to force home owners to publicly declare the amount for which their homes sell. If a person really wants to know the price for which a home sells, they can attend the auction,'' Mr Raimondo said.

But buyers advocate Christopher Koren said many agents were resorting to ''sneaky behaviour'' to mislead buyers over the true state of the market and that mandatory reporting was ''an obvious and necessary reform''.

Why would they withold the information it if it didn't indicate the shit was hitting the fan?

No comments:

Post a Comment