Leith Van Onselen (aka Unconventional Economist) at Macrobusiness wrote a corker today demonstrating why Property prices have hit the ceiling and cannot outsrip incomes. You can read it here.

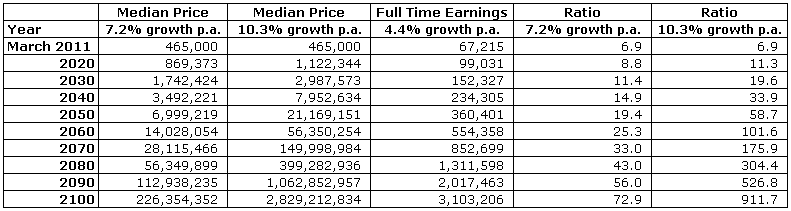

Ah yes, the tired old property doubles every seven to 10 years myth. To illustrate the absurdity of Mr Armstrong’s claim, I took Melbourne’s median dwelling price ($465,000) against Australia’s average full-time earnings ($67,215) as at March 2011. I then used the Rule of 72 to extrapolated the house prices forward by 7.2% and 10.28% per annum respectively (i.e. the growth rates required to double every seven or 10 years), and extrapolated average full-time earnings forward by 4.4% per annum, which is the average rate of growth since 1990. The results are presented in the below table.

Click on graph to expandAs you can see, a growth rate of 7.2% per annum delivers a median dwelling price of around $226 million in the year 2100 against an average income of around $3.1 million, producing a dwelling price-to-income ratio of nearly 73 times!A growth rate of 10.3% per annum delivers a median dwelling price of around $2.8 billion in the year 2100 against an average income of around $3.1 million, producing a dwelling price-to-income ratio of nearly 912 times!Clearly Mr Armstrong does not understand the laws of compounding. In fact, the only way that his ‘doubles every seven to 10 years’ claim could ever be met is if the Reserve Bank and Government abandoned inflation targeting and allowed both wages and house prices to grow in concert via inflation (like in the 1970s). In such an event, the dwelling price-to-income ratio would be largely unchanged, but house prices could continue growing strongly in nominal terms whilst remaining steady in real terms.

I, however, disagree with his opinion that Australian will not crash (like Ireland, Spain, USA etc). Thats fine, opinions are like arses, we all have one.

History shows that bubbles don't flatline, they deflate.

I wrote about this in April - History Never Repeats.

Consider a fall of just 0.8% a month will give you a -32% haircut over 4 years. Is that a crash? Call it whatever - it won't be pretty and it WILL take out some of the banking sector.

Don't forget the optimism of US Fed's Bernanke:

2/15/06 – Hearing before the Committee on Financial Services

“Housing markets are cooling a bit. Our expectation is that the decline in activity or the slowing in activity will be moderate, that house prices will probably continue to rise.”2/15/07 - Semiannual Monetary Policy Report to the Congress

“Despite the ongoing adjustments in the housing sector, overall economic prospects for households remain good. Household finances appear generally solid, and delinquency rates on most types of consumer loans and residential mortgages remain low.”

No comments:

Post a Comment